{kind=link}

[ad_1]

It’s everybody’s favourite time of the 12 months: tax season! Okay…which may be an exaggeration, however both means, it’s probably that you’ll come throughout tax phrases that will have you ever scratching your head.

Taxes are a certainty yearly, so having a greater understanding of some jargon could make the entire subject rather less daunting.

Navigating the U.S. Federal Earnings Tax System

You’re NOT alone if you happen to don’t know the distinction between your marginal and efficient tax charge. Nonetheless, understanding these charges is important for efficient tax planning.

Together with gaining perception into how a lot of your revenue goes to taxes, you’ll additionally be capable to make higher selections round tax planning alternatives.

Marginal tax charge

The U.S. federal revenue tax system is progressive. This implies tax charges enhance as your taxable revenue will increase.

The tax bracket into which your final greenback of revenue falls determines your marginal tax charge. Nonetheless, you don’t pay that increased marginal tax charge in your whole revenue. You solely pay the upper charge on the portion of revenue that really falls inside that high tax bracket. The revenue earned within the decrease brackets will get taxed on the corresponding decrease charges.

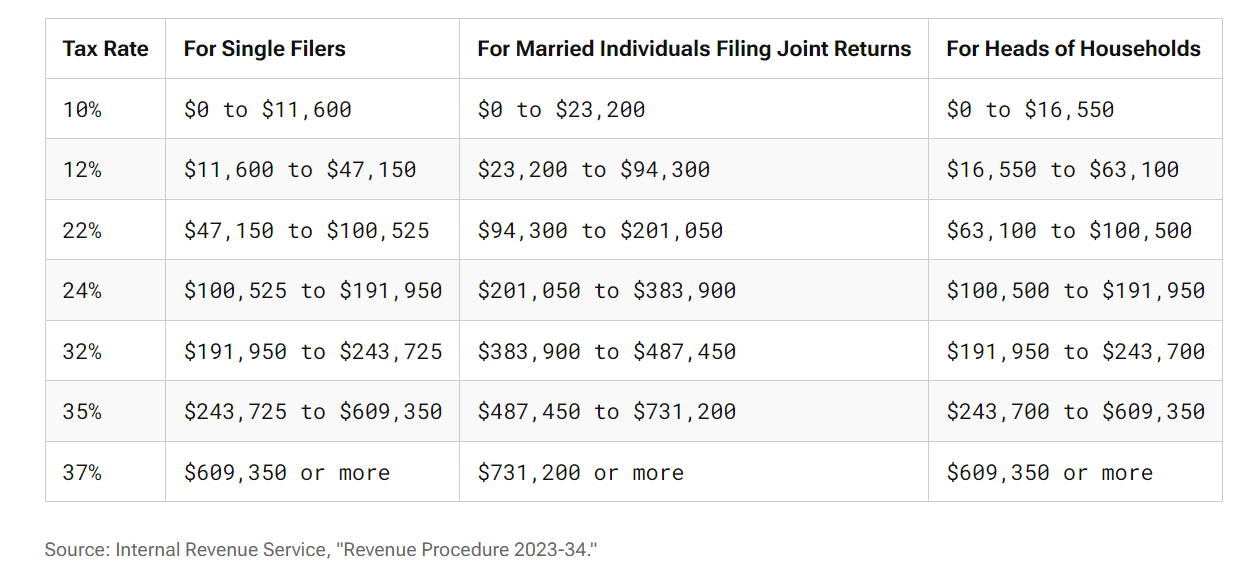

The tax brackets for 2024 are as follows:

Examples of marginal tax charges in motion

Let’s check out a easy instance utilizing 2024 figures to assist clarify this idea additional:

- Tax Submitting Standing: Married Submitting Collectively

- Complete Gross Earnings (earlier than making use of any deductions): $220,000

- Commonplace Deduction (itemized deductions had been decrease so the usual deduction was claimed): $29,200

- Taxable Earnings: $190,800

Primarily based on the 2024 tax brackets, you’d pay:

- 10% in your first $23,200 of revenue: $2,320

- 12% in your subsequent $71,100 of revenue ($94,300 – $23,200): $8,532

- 22% in your subsequent $96,500 of revenue ($190,800 – $94,300): $21,230

- Complete tax due: $32,082

Your marginal, or highest, tax charge could be 22% on this instance.

Marginal tax charges serve an vital function if you end up ensuring tax-management selections, like if it is smart to do a Roth conversion for example, amongst different planning alternatives.

For those who head over to Insights > Taxes within the NewRetirement Planner, the Internet Taxable Earnings by federal Tax Bracket chart gives you a greater concept of the margin tax charge that applies to your particular monetary scenario.

Efficient tax charge

Whereas your marginal tax charge represents the best tax bracket your taxable revenue places you in, the efficient tax charge is the overall greenback quantity of your tax legal responsibility as a proportion of your taxable revenue. In different phrases, it’s the typical tax charge that you simply pay on all your taxable revenue.

Your efficient tax charge is the overall quantity you pay in taxes for the 12 months divided by your taxable revenue:

Efficient tax charge = Complete tax ÷ Taxable revenue

Going again to the instance above for calculating your marginal tax charge:

- Taxable Earnings: $190,800

- Complete Tax Due: $32,082

- Efficient Tax Charge ($32,082 ÷ $190,800) = 16.8%

On this instance, the marginal tax charge was 22%, however the efficient tax charge is decrease, at 16.8%.

Efficient tax charges are useful in gaining a greater understanding of the share of your whole revenue that’s allotted to taxes.

Making Sense of Tax Documentation

If the concept of making ready your tax return isn’t already anxiety-inducing sufficient, receiving or coming throughout mysterious tax doc lingo doesn’t mitigate these emotions.

Kind W-4

For those who’re employed in the US, you’re probably conversant in the W-2 tax type, which you obtain early within the 12 months and summarizes your annual earnings and the taxes deducted by your employer for federal, state and native functions.

In the meantime, the Kind W-4, an IRS doc, is crammed out if you end up an worker to information your employer on how a lot federal tax needs to be withheld from every paycheck. Finishing this kind precisely is important because it prevents each overpayment, rising your take-home pay, and underpayment, avoiding stunning tax payments or penalties.

It’s not unusual to fill out a W-4 as a brand new rent after which by no means come throughout it once more. Nonetheless, there are occasions the place it could actually make sense to revisit the W-4, corresponding to:

- A change in tax submitting standing (e.g. married submitting collectively to single)

- Acquiring a second job

- Going from a dual-income family to single revenue family

- A brand new addition to the household (e.g. beginning of a kid)

- Eligibility for substantial tax credit

- Shopping for a brand new dwelling

Revising a W-4 can really feel daunting, however there are useful assets on the market to help with the method. Preserving your Kind W-4 up to date ensures that your withholding precisely displays your present tax scenario.

1099

Submitting your taxes is rarely an thrilling exercise to stay up for every year. Whether or not you’re employed with a tax skilled or deal with it by yourself, it may be demanding gathering the required paperwork to arrange your taxes precisely, particularly when chances are you’ll not have a full understanding of the paperwork you’re receiving.

A typical tax doc is a Kind 1099. This tax doc reviews revenue you obtain from sources aside from an employer. There are lots of various kinds of 1099 kinds, every with its personal distinctive reporting necessities.

The most typical varieties of 1099 kinds embody:

- 1099-DIV: revenue obtained by way of dividends and different inventory distributions (typically $10 or extra)

- 1099-INT: curiosity revenue from a financial institution or one other monetary establishment (typically $10 or extra)

- 1099-B: proceeds from the sale of shares, mutual funds, ETFs and different varieties of monetary transactions, plus the sale date and different info

- 1099-R: distributions from pensions, annuities, retirement or profit-sharing plans, IRAs, and insurance coverage contracts and can present info on any taxes withheld from the distribution

- 1099-SA: withdrawals out of your HSA (distributions for certified medical bills aren’t taxable)

You need to look out for the 1099s which can be relevant to your monetary scenario in January and February of every 12 months as these are important tax paperwork in making ready an correct tax return.

NOTE: Reviewing your 1099 from a taxable funding account may be useful in making use of an applicable turnover charge for tax functions to all these accounts within the NewRetirement Planner.

Decreasing Your Tax Invoice

A deduction, a credit score…it could sound easy however until you’ve not too long ago attended an accounting class, it’s value revisiting these frequent phrases chances are you’ll come throughout when discussing reducing your taxes.

Tax deductions

Who doesn’t like speaking about lowering your tax invoice?

One of many methods to do that is thru a tax deduction, which is an expense that may scale back your taxable revenue, subsequently lowering your total tax legal responsibility. Tax deductions are subtracted out of your revenue earlier than taxes are calculated, which reduces the quantity of revenue that’s topic to taxation.

There are two principal varieties of tax deductions:

- Commonplace Deduction: A set greenback quantity set by the IRS that may be claimed once you do not need sufficient certified bills to itemize

- In 2024, the usual deduction varies primarily based in your submitting standing with Single and Married Submitting Individually at $14,600, Married Submitting Collectively at $29,200 and Head of Family at $21,900

- People over age 65 could declare a further customary deduction of $1,950 for single or head of family filers and $1,550 for married submitting collectively or individually filers

- Itemized Deductions: Particular bills that may be claimed in your tax return, like medical and dental bills and mortgage mortgage curiosity, amongst others

The Planner estimates if you happen to could be higher off itemizing deductions or utilizing the usual deduction each on the Federal and State ranges in every year of the simulation.

Whereas tax deductions scale back your taxable revenue, a tax credit score may be much more priceless, which we’ll focus on subsequent.

Tax credit scores

A tax credit score is one other helpful instrument for lowering your total tax legal responsibility.

A tax credit score instantly reduces the quantity of tax you owe. It’s a dollar-for-dollar discount of your precise tax invoice, making it an much more priceless instrument than a deduction for minimizing your tax obligation.

There are two major varieties of tax credit:

- Refundable: scale back your tax legal responsibility to under zero, which suggests chances are you’ll obtain a refund

- Non-refundable: scale back your tax legal responsibility to zero however can’t lead to a refund

Tax credit range extensively, each by way of their quantity and kinds, and these can change from one tax 12 months to the following. It’s vital to completely overview any relevant tax credit if you end up making ready to file your annual tax return.

Contemplate Taxes as A part of Your Charitable Giving Technique

Who wouldn’t need to give to charity and in addition save on taxes? It’s a win-win scenario! However, in fact, there’s a variety of totally different terminology in relation to saving taxes by way of charitable giving instruments.

Donor Suggested Fund (DAF)

For those who’re feeling charitably inclined and have explored totally different avenues for giving, you might have come throughout info on a Donor Suggested Fund, or DAF.

With a Donor Suggested Fund, you identify an account, contribute funds, after which determine on the funding technique whereas additionally initiating grants to chosen charities. The grants should be directed to certified charitable organizations, and you’ve got the flexibleness to rearrange one-time presents or recurring presents. For instance, you would deposit $20,000 into the fund and elect that you simply want to distribute $5,000 to your chosen charities over a span of 4 years.

Once you make a contribution to your DAF, you get a direct tax deduction. This profit may be significantly priceless in years when your taxable revenue is increased. By doing so, chances are you’ll surpass the usual deduction threshold and itemize your deductions to additional decrease your tax invoice for the 12 months.

DAFs supply a versatile, straightforward to arrange and cost-effective strategy to charitable giving.

Certified Charitable Distribution (QCD)

One other frequent technique for charitable giving is a Certified Charitable Distribution, or QCD.

With a QCD, you’re taking a distribution out of your IRA and giving it on to a certified charitable group. The distribution should be made instantly by the trustee of the IRA to the charity. An IRA distribution, like an digital fee made on to the IRA proprietor, doesn’t depend as a QCD.

In 2024, people aged 70.5 and older can contribute as much as $105,000 per 12 months to a number of charities. For a married couple, if each spouses are age 70.5 or over when the distributions are made and each have IRAs, every partner can exclude as much as $105,000 for a complete of as much as $210,000 per 12 months.

A QCD is a priceless technique from a tax standpoint for the next causes:

- You don’t report QCDs as taxable revenue

- You don’t owe any taxes on the QCD, even when you don’t itemize deductions

- You’ll be able to fulfill your annual Required Minimal Distribution (RMD)

- You’ll be able to scale back RMDs in future years by lowering the steadiness of the IRA

NOTE: When selecting to make a QCD, verify the receiving group is certified to just accept QCDs.

Simplifying Tax Lingo Associated to Investments

It’s vital to maintain investing easy, however it may be tough when taxes come into play with most funding selections.

Tax-loss harvesting

Tax-loss harvesting is a possible technique referring to investments inside a taxable brokerage account.

It entails promoting investments which have decreased in worth or are underperforming, thereby realizing a capital loss, and changing the funding with a extremely correlated various. You’d then use that loss to offset any realized capital beneficial properties from promoting different investments, with the purpose of lowering your total tax legal responsibility.

If there are not any realized capital beneficial properties to offset, as much as $3,000 per 12 months in funding losses can be utilized to offset your wages, taxable retirement revenue and different peculiar revenue (for married people submitting individually, the deduction is $1,500). For those who notice greater than $3,000 in losses in a single 12 months, you may carry over the surplus quantity to offset capital beneficial properties and revenue in future years.

Wash sale

It wouldn’t be prudent to speak about tax-loss harvesting with out being conscious of the wash sale rule.

The wash sale rule prohibits the promoting of securities, corresponding to shares or bonds, at a loss, shopping for again those self same or “considerably similar” shares inside 30 days earlier than or after the sale, and deducting such loss for revenue tax functions. Because it’s 30 days earlier than or after the sale, it’s truly a 60-day prohibited interval throughout which the loss will not be deducted.

For those who’re excited about tricking the IRS by together with your partner within the transaction, suppose once more! The wash-sale rule applies to each you and a partner as if you happen to had been a unit. For instance, if you happen to’re considering of promoting a safety in a taxable brokerage account at a loss after which having your partner purchase it again of their IRA, it might nonetheless be thought-about a wash sale.

The aim of the wash sale rule is to discourage you from promoting securities to take a tax loss after which turning proper round and shopping for them again.

Preserve Up-to-Date with Tax Laws

Together with tax jargon, to make issues much more advanced, tax legal guidelines at all times appear to be altering from 12 months to 12 months. It’s vital to pay attention to potential adjustments to your tax scenario on the horizon.

The Tax Cuts and Jobs Act (TCJA)

In 2017, the Trump administration signed into legislation a big piece of tax laws, The Tax Cuts and Jobs Act (TCJA).

TCJA caused intensive revisions to the U.S. tax code, together with quickly reducing particular person revenue tax charges, a rise in the usual deduction, a discount within the company tax charge, and adjustments to varied deductions and credit.

Except Congress takes motion, a number of of the non permanent adjustments introduced on by TCJA for particular person taxpayers are set to run out on December 31, 2025. One of many larger adjustments would contain the person tax charges reverting to their 2017 ranges:

- The 12% charge may return to fifteen%

- The 22% charge may return to 25%

- The 24% charge may return to twenty-eight%

- The 32% charge may return to 33%

- The 37% charge may return to 39.6%

Given taxes play such a necessary function in your retirement planning, the NewRetirement Planner lets you swap between and simulate numerous projections utilizing both the present decrease tax charges or the potential return to the upper charges, beginning in 2026.

Study extra about TCJA or check out the tax charge toggle within the NewRetirement Planner in My Plan > Assumptions.

Achieve Insights on Your Tax State of affairs with the NewRetirement Planner

With a greater understanding of some tax phrases, chances are you’ll really feel extra outfitted to deal with your taxes this 12 months. Nonetheless, tax planning isn’t a one and achieved occasion; it’s an ongoing course of.

The NewRetirement Planner allows you to see your potential tax burden in all future years and get concepts for minimizing this expense. As your understanding of taxes deepens, you’ll really feel extra empowered and assured concerning the success of your monetary plan.

[ad_2]