{kind=link}

[ad_1]

Save, save, save! Chances are you’ll really feel like that’s all you hear once you’re researching how you can plan in your retirement if you are nonetheless working.

It’s good, easy recommendation, however there’s a lot extra to financial savings than to “simply save extra”. What accounts must you save to? What are the advantages of saving to at least one vs. the opposite? What tax implications must you pay attention to? How a lot must you be saving?

With a purpose to optimize your financial savings if you are nonetheless within the accumulation part (i.e. working and nonetheless contributing to your investments), it’s important to suppose by some of these questions so you’ll be able to have one of the best plan tailor-made to your distinctive monetary state of affairs.

1. Construct a Robust Monetary Basis

Earlier than we dive deeper into optimizing your financial savings, it’s important that you’ve a stable monetary basis in place. Though these options could seem as fundamental as ABC, your private funds are off to a powerful begin in the event you can verify these three objects off your record.

A) Preserve a stash of emergency financial savings

This may shock you, however earlier than you save for retirement, you must construct up a stash of emergency financial savings. Emergency financial savings are the muse of monetary safety.

An emergency fund, cash sometimes held in simply accessible accounts like a high-yield on-line financial savings account or cash market fund, is important for coping with unanticipated bills or occasions equivalent to a job loss, costly dwelling restore or massive medical invoice. As everyone knows, life is extraordinarily unpredictable and issues are likely to pop up unexpectedly, so your emergency fund serves as a monetary security web to assist navigate this uncertainty.

Be taught extra about how a lot you must have.

NOTE: You possibly can earmark your emergency fund within the NewRetirement Planner as an account you don’t need to use as a part of your withdrawal technique in retirement. This may be performed underneath My Plan > Accounts and Property. In case you have a selected financial savings account for emergencies solely, you’ll be able to hit the Pencil Edit icon and choose ‘Sure’ for ‘Exclude this account out of your withdrawal methods?’

B) Get the FREE cash, seize employer match

Employer match refers to a profit supplied by some employers whereby they contribute a sure amount of cash to their workers’ retirement financial savings plans, equivalent to a 401(okay) or 403(b), typically it’s based mostly on the quantity the worker contributes. The employer sometimes matches a proportion of the worker’s contributions, as much as a sure restrict.

Employer match is actually free cash.

You’ll need to perceive how a lot your organization matches your retirement contributions (in the event that they match in any respect). Many firms sometimes match 100% of your individual contribution, usually as much as a specified most proportion of your wage, which tends to be throughout the vary of three% to six%. This matching formulation will differ by plan so you should definitely make clear along with your employer.

It’s additionally tremendous essential to grasp your organization’s retirement plan vesting schedule. Typically, you’ll must be at your organization for about three years to be absolutely vested, which means that cash is yours in the event you resolve to maneuver on. That is additionally a plan-specific function, so you should definitely confirm these particulars along with your employer. Your individual contributions, nonetheless? These are yours, it doesn’t matter what!

The important thing takeaway right here is to goal to contribute sufficient to your office retirement plan to snag that full employer match.

NOTE: See the affect of an employer match by incorporating it into your NewRetirement Plan. Employer contributions to your retirement plan will be added underneath My Plan > Earnings > Work. You can too now add contributions your employer is making to your retirement plan regardless in the event you contribute or not (i.e. a non-elective contribution).

C) Repay high-interest money owed

Wait, paying off debt isn’t saving. True, however in case you have emergency financial savings and are capturing employer match, your subsequent precedence actually needs to be paying off high-interest debt.

Whenever you’re investing within the inventory market, nothing is a assure. In the meantime, paying off high-interest price debt, like a bank card for instance, is a assured funding return.

A assured funding return signifies that once you put money in the direction of debt, your return is the same as the rate of interest on that debt. So, once you use money to repay your bank card with an rate of interest of twenty-two%, you’re immediately incomes a 22% funding return. Who doesn’t love a assured return within the double digits?

The upper the rate of interest on the debt, the extra you save once you lower your debt. Concentrate on paying off these pricey money owed with excessive rates of interest earlier than optimizing your retirement financial savings.

2. Save AND Make investments

It isn’t sufficient to simply save. For all the things however your emergency financial savings (which needs to be held in a liquid or simply accessible account), it would be best to make investments.

Investing permits you to reap the benefits of compounding returns. Your cash will develop with none extra work from your self.

3. Take into account Following the Financial savings Playbook

Look, there’s a lot to contemplate relating to saving. You could have competing objectives. To make it easy, begin with the ABCs listed above after which proceed to knock off different financial savings objectives, a lot of that are coated in additional element under.

CHART

4. Have a Stable Concept of How A lot Retirement Financial savings You Are Going to Want

You’ve probably encountered numerous guidelines of thumb relating to retirement financial savings and desires:

- Save 15-20% of your gross earnings in the direction of retirement, together with any employer match

- Amass 25x your deliberate annual spending by retirement

- The 4% rule

Or maybe you landed on an arbitrary variety of $1,000,000, $3,000,000, and even $10,000,000? Perhaps a pal or neighbor instructed you that’s what their “monetary man or gal” instructed them they should should retire.

The principles of thumbs are nice beginning factors and simplify whether or not you might be on observe or not. However to reply the query for your self, it pays to dig deeper.

There’s so many alternative variables to contemplate based mostly in your distinctive state of affairs:

- Did you begin saving at 25 or at 40?

- Do you spend $5,000/month or $15,000/month?

- Are you invested in 100% bonds or 100% shares?

- Do you anticipate an inheritance of $1,000,000 or none in any respect?

- Do you intend on working till 70 or need to cease fully at 50?

- Are you planning on retiring in California or Panama?

The excellent news is the NewRetirement Planner will will let you plan step-by-step and present you the way a lot financial savings you have to. By getting into in your present and projected earnings sources, contributions and bills, in addition to assumptions like inflation and funding returns, you’ll achieve peace of thoughts from seeing an in depth plan.

Take quite a lot of the guesswork out of it and make your self a written plan. You received’t remorse it!

5. Automate Your Financial savings

Autmating financial savings refers tothe observe of establishing automated transfers or contributions out of your paycheck into your financial savings accounts.

Automating your financial savings is a good suggestion as a result of it ensures:

- Consistency: By automating your financial savings, you guarantee an everyday financial savings behavior, making it simpler to realize your monetary objectives over time.

- Self-discipline: Automation removes the temptation to spend the cash earmarked for financial savings. For the reason that funds are transferred robotically earlier than you’ve an opportunity to spend them, you’re much less prone to dip into your financial savings for discretionary bills.

- Aim Achievement: Common contributions add up over time, serving to you attain your targets quicker.

6. Take Benefit of Completely different Tax Buckets

Now that now we have the fundamentals out of the way in which, it’s time to delve deeper into the numerous various kinds of accounts you might have entry to as a part of your retirement financial savings.

A) Know your tax buckets

You possibly can consider taxable, tax-deferred and tax-exempt accounts as three “tax buckets”:

- Taxable accounts: Taxable accounts could embrace particular person and joint brokerage accounts or trusts and shouldn’t have particular tax benefits.

- The cash you set right into a taxable account is after-tax cash. After-tax cash is cash that has already been taxed and the rest is out there to spend or save.

- You additionally pay tax on the expansion. Curiosity and dividends that your funds generate and any capital positive aspects you notice, are taxable within the 12 months by which they happen.

- Curiosity, non-qualified (odd) dividends and short-term capital positive aspects are taxed at odd earnings charges whereas realized long-term capital positive aspects and certified dividends are taxed at preferential charges.

- Tax-deferred accounts: Tax-deferred accounts embrace conventional IRAs, 401(okay)s and extra. These financial savings automobiles provide you with speedy tax benefits.

- They’re funded with pre-tax cash. You make investments your earnings with out having to pay taxes on these funds.

- Development is tax-deferred, which suggests you solely pay taxes once you withdraw the cash.

- Tax-exempt accounts: Tax-exempt accounts embrace Roth IRAs, Roth 401ks, and others. These accounts provide you with future tax benefits.

- They’re funded with after-tax cash, which means cash you’ve paid taxes on.

- Neither progress nor certified distributions are taxed.

Now that you’ve a greater understanding of how sure accounts match into every tax bucket, let’s discover how one can maximize your financial savings potential utilizing these numerous forms of accounts.

B) Range Throughout Taxable, Tax-Deferred and Tax-Exempt Accounts

In fact, taxes are all the time essential to remember when you find yourself making selections about optimizing your financial savings. Sustaining a diversified portfolio of taxable, tax-deferred and tax-exempt accounts gives flexibility in how your withdrawals are taxed throughout retirement.

7. Get Triple-Tax Benefits with a Well being Financial savings Account (HSA)

Upon getting a totally funded emergency fund, paid off pricey high-interest debt, and are benefiting from your employer match, a Well being Financial savings Account could also be your subsequent finest choice to optimize your retirement financial savings.

Most funding accounts match neatly into one of many three tax buckets mentioned above. Nonetheless, the Well being Financial savings Account is a novel account (in a great way!) that mixes a few of the tax benefits of assorted buckets.

What’s a Well being Financial savings Account? A Well being Financial savings Account (or HSA) is a kind of financial savings account that’s used to pay for eligible medical bills. Nonetheless, eligibility for opening an HSA isn’t open to everybody. To qualify, you should be enrolled in a high-deductible medical health insurance plan (HDHP) as outlined by the IRS.

Contributions to an HSA are solely permitted when you’re actively enrolled in a HDHP. Nonetheless, even in case you are not part of a HDHP, you’ll be able to nonetheless reap the benefits of any stability throughout the HSA and use the funds for certified medical bills.

Advantages of Funding an HSA: With an HSA, you’ve two major paths for making contributions:

- Pre-tax payroll deductions by an employer

- Submit-tax contributions to an HSA not tied to your employer and claiming a tax-deduction your tax return

Both manner, you don’t pay any earnings tax on the {dollars} you contribute to your HSA (tax profit #1!).

After you contribute to an HSA, it’s possible you’ll need to make investments these contributions for long-term progress in the event you plan on paying for ongoing medical prices out-of-pocket whereas working. With an HSA, you don’t pay any taxes on capital positive aspects, dividends, or curiosity whereas holding or promoting your investments (tax profit #2!).

And once you withdraw cash from the HSA to pay for certified medical bills, you don’t owe any taxes (tax profit #3!).

When you attain 65, you’ve the choice to withdraw funds from the HSA with out penalty, no matter whether or not they’re used for certified medical bills. Nonetheless, withdrawals for non-medical bills are nonetheless topic to earnings taxes, though the penalty of 20% that applies earlier than age 65 is waived.

2024 Contribution Limits: For 2024, people underneath a excessive deductible well being plan (HDHP) have an HSA contribution restrict of $4,150.

The restrict for household protection is $8,300. If you’re 55 or older, you’ll be able to contribute a further $1,000. These limits embrace any employer contributions as effectively.

8. Max Out Your Employer Retirement Plan Contributions

We mentioned earlier how you must contribute sufficient to your employer retirement plan to get any employer match, however you don’t need to cease there!

Your subsequent focus needs to be on rising these contributions as a lot as doable till you hit the utmost for the 12 months. A 1-2% improve in your contribution every year, or everytime you obtain a elevate, pays big dividends over the long-term.

9. Know Whether or not to Save in Pre-Tax or Roth

It’s by no means so simple as simply making one kind of contribution to your employer retirement plan, although. There’s choices, in fact.

Pre-tax vs. Roth contributions

For a lot of people, you might have a 401(okay) or a 403(b) plan by your employer.

For some of these plans, you usually have the choice to contribute on a pre-tax foundation and/or a Roth foundation. The distinction in contributions are as follows:

- Pre-tax: tax deduction once you contribute, pay taxes once you withdraw later in retirement

- Roth: no tax deduction once you contribute, however certified distributions are tax-free in retirement

When pondering by whether or not to make pre-tax or Roth contributions:

- Contribute on a pre-tax foundation: you consider you can be in a decrease tax bracket when withdrawing cash in retirement vs. now

- Contribute on a Roth foundation: you consider you can be in a better tax bracket when withdrawing cash in retirement vs. now

Given we don’t know what the long run holds precisely for tax laws, brackets and charges, deciding whether or not it is sensible to make pre-tax or Roth contributions will be troublesome. Nonetheless, it doesn’t should be an both/or determination. You are able to do each, as effectively (assuming your plan permits Roth contributions)!

NOTE: You possibly can mannequin making pre-tax, Roth or a mixture of pre-tax and Roth contributions within the NewRetirement Planner to see the affect in your long-term monetary plan.

After-tax contributions

Your employer plan may additionally supply the power to make after-tax contributions.

Typically, after-tax contributions are a consideration after maxing out your pre-tax and/or Roth contributions for the 12 months.

When you received’t get a tax deduction for an after-tax contribution, contributions are tax-free at withdrawal, however any earnings generated on these contributions are taxed as odd earnings on the time of distribution.

With cash in an after-tax account, your plan may additionally allow you to reap the benefits of a Mega backdoor Roth technique.

A mega backdoor Roth technique is when, after making after-tax contributions, you change the contributions instantly to a Roth 401(okay) or Roth IRA. This fashion, each the after-tax contributions and the earnings can be tax-free in retirement, vs. simply the contributions (when making after-tax contributions and leaving them as is).

Verify along with your HR division to make sure you can implement one of these technique as a result of your plan has to supply both in-service (whereas working) distributions to a Roth IRA or the power to maneuver cash from the after-tax portion of your plan into the Roth 401(okay) a part of the plan (if there’s one).

2024 contribution limits

For 2024, the restrict for pre-tax and/or Roth contributions to 401ks, 403bs, most 457s in addition to Thrift Financial savings Plans is $23,000. And, in case you are 50 or older, the catch-up contribution is a further $7,500. So, it can save you a complete of $30,500!

In case your employer retirement plan permits for after-tax contributions, the utmost that you simply and your employer mixed can put into your plan is $69,000, or $76,500 for people 50 and older in 2024.

10. You Aren’t Restricted to Employer Financial savings: Max Your Financial savings Outdoors of Your Employer

Not your entire retirement financial savings should be by your employer plans. Together with an employer retirement plan or a Well being Financial savings Account, you might also have an IRA or taxable brokerage account that may play a big position in your annual financial savings plan.

Conventional IRA

Whenever you make a contribution to a conventional IRA, you’ve the potential to obtain a tax deduction in your contribution, your cash grows tax-deferred, and distributions from the account can be hit with odd earnings tax. The utmost you’ll be able to contribute to an IRA (Conventional or Roth) in 2024 is $7,000 ($8,000 for people 50 or older).

There are, nonetheless, limits on the deductibility of IRA contributions. If through the 12 months both you or your partner was coated by a retirement plan at work, the deduction could also be lowered, or phased out, till it’s eradicated, relying on submitting standing and earnings:

- Single Filers: Modified Adjusted Gross Earnings (MAGI) between $77,000 and $87,000

- Married Submitting Collectively: if the partner making the IRA contribution is roofed by a office retirement plan, MAGI between $123,000 and $143,000

- Married Submitting Collectively (IRA contributor will not be coated by office retirement plan however partner is): MAGI between $230,000 and $240,000

- Married Submitting Individually: MAGI between $0 and $10,000.

If neither you nor your partner is roofed by a retirement plan at work, the phase-outs of the deduction don’t apply.

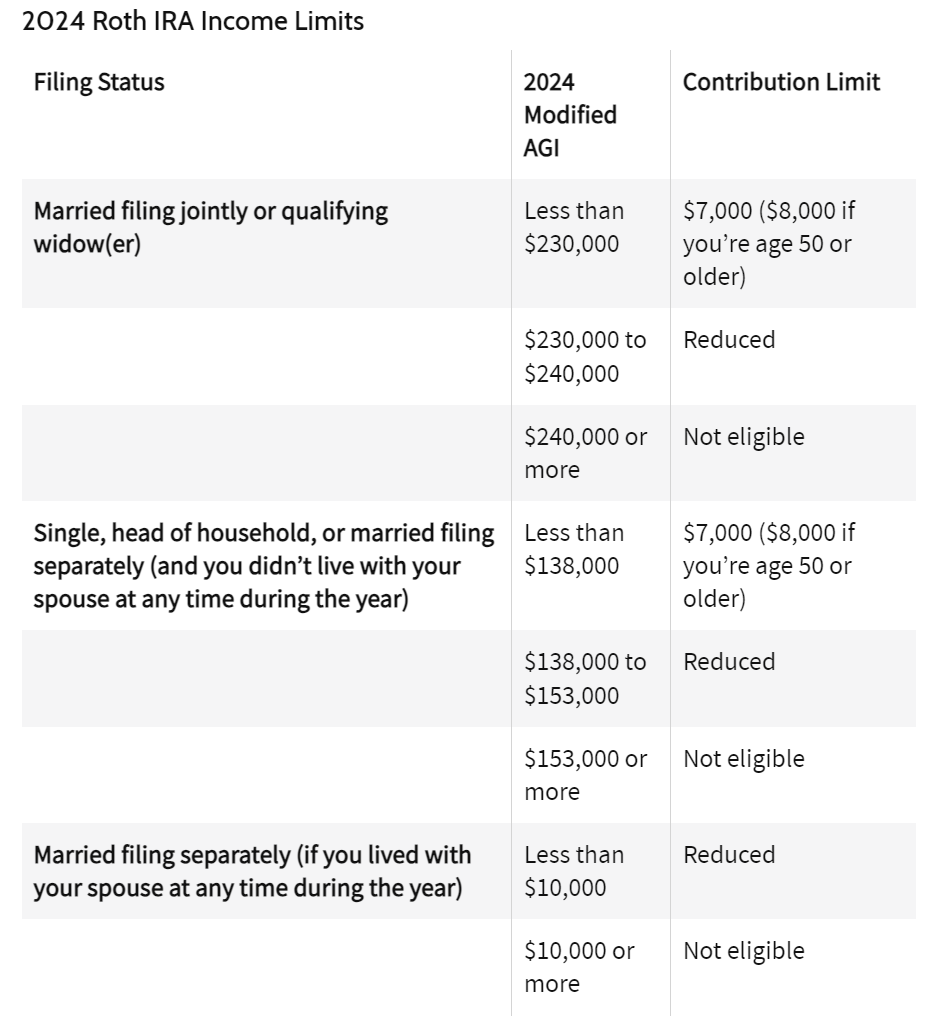

Roth IRA

Whenever you make a contribution to a Roth IRA, you might be placing cash into the account after paying earnings tax on it, after which these {dollars} develop tax-free and will be withdrawn tax-free.

Nonetheless, there are earnings limits that prohibit who can contribute on to a Roth IRA:

11. Take into account a Backdoor Roth IRA Technique

Should you earn an excessive amount of to contribute on to a Roth IRA, given the earnings limits above, it’s possible you’ll think about a backdoor Roth IRA technique.

This includes making a non-deductible Conventional IRA contribution after which making a subsequent conversion to a Roth IRA account.

Nonetheless, earlier than contemplating this technique, you’ll need to pay attention to the IRS’ pro-rata rule. This rule requires you to contemplate ALL of your IRAs as the identical account. Subsequently, in case you have a Conventional IRA, SIMPLE IRA or SEP IRA, these balances are thought of relating to figuring out your tax owed on the conversion. So, in case you have a stability in any of some of these accounts on the finish of the 12 months, it’s possible you’ll need to rethink a backdoor Roth IRA technique.

Taxable Accounts

After exhausting your tax-advantaged accounts above, as a excessive earner or super-saver, it’s possible you’ll think about a taxable account, like a person or joint brokerage account, subsequent.

Taxable brokerage accounts do supply quite a lot of flexibility in that there aren’t any contribution or earnings limits like a lot of the accounts we’ve mentioned up till now. You can too promote and take the cash each time it is advisable to!

Whereas taxes on dividends and capital positive aspects are inevitable every year, adopting a low-cost, hands-off funding technique can nonetheless imply comparatively minimal taxes and foster long-term progress in your contributions.

NOTE: Contemplating tax mitigation methods equivalent to asset location and tax loss-harvesting is important when investing in taxable accounts.

12. Construct and Preserve a Holistic Monetary Plan

It’s probably that you simply attempt to eat effectively, train repeatedly, socialize with associates, and work, learn books, or interact in different actions that hold your mind working effectively. These are all actions associated to “wellness.”

However, do you even have habits and a observe round your monetary life? Private finance is a essential element of your total effectively being. Constructing and sustaining a private monetary plan for all facets of your cash is a good first step to taking management of your monetary life.

Use the NewRetirement Planner to take management and construct the habits you want for higher monetary selections, confidence, safety, and peace of thoughts.

[ad_2]